Imagine that it’s time to file expenses. Instead of logging into a portal, uploading photos of your crumpled receipts, filling out 10 information fields, and then waiting a week for your manager to sign off, you simply answer a text with a photo of a receipt and a short note about what it’s for.

Done.

“That is, to me, the golden experience,” says Diego Zaks, VP of design at Ramp, the $22.5 billion fintech company that’s reinventing the business expense landscape.

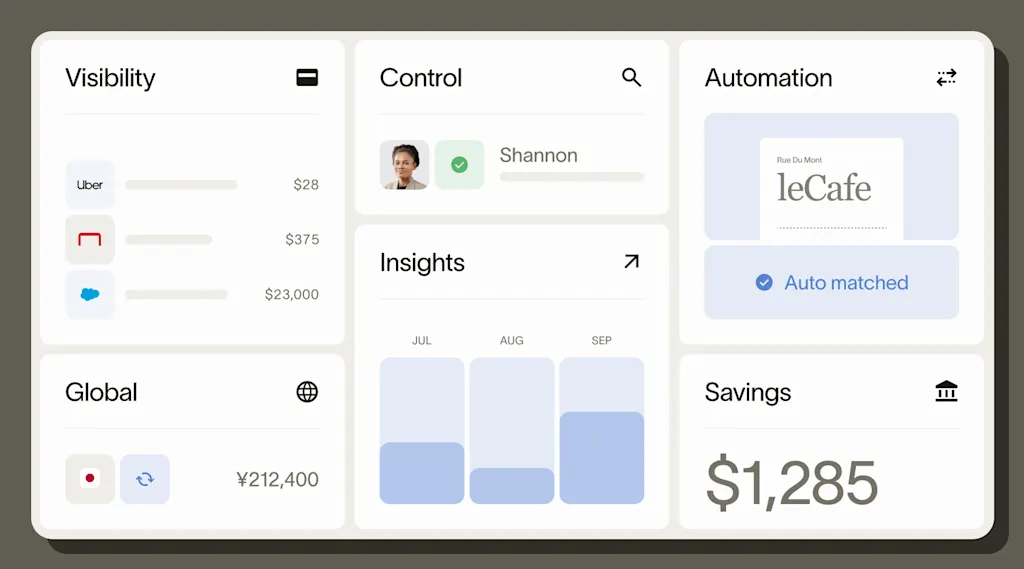

Ramp as a platform is in the business of simplifying. It consolidates corporate cards, expense management, bill payments, and accounting automation into a single system, making it easier for companies to track expenses and keep their finances in order.

In the era of AI, Zaks believes the company can do even more to simplify the software for the people who use it. He envisions a world where Ramp’s customers can accomplish any task with the push of a single button. And his ultimate goal? Someday you’ll forget altogether that you’re using Ramp.

“I don’t want anyone using Ramp—because every minute that you’re on Ramp, it’s a minute that you’re dealing with expenses and not actually doing the job that you’re hired to do,” he explains. “We actually measure engagement and time spent on Ramp going down as the signal that we are trying to get.”

A better AI agent

In July, Ramp introduced Ramp Agents, an autonomous, AI-driven system built atop OpenAI’s latest reasoning models. Ramp Agents work behind the scenes to review expenses, enforce company spend policies, and even suggest improvements to those policies—without users needing to intervene or monitor every transaction manually.

Instead of relying on rigid rules or requiring employees to learn new workflows, these agents reason through real business context, handling approvals, flagging anomalies, filling forms, and learning from every bit of feedback. They don’t require a prompt to do things; instead, they do everything on their own, so people interact as little as possible, if at all.

“People didn’t come to Ramp to engage with AI—they come to do a specific job, and we have AI in the background doing 90% of that job or as much of that job as we possibly can and just displaying the outcome,” Zaks says. “We skip 17 steps and we just got [managers] to the last moment of ‘Does this look good?’ And they can just say yes, and it’s done.”

The agents are part of Ramp’s larger ecosystem. When companies sign up for Ramp, they receive corporate charge cards with preconfigured spending policies and limits. Employee transactions trigger receipt capture through email integrations, mobile apps, or merchant partnerships with Amazon Business, Lyft, and Uber. The system categorizes expenses, enforces policies in real time, and flags violations automatically.

Zaks believes that when deployed smartly, agents will be able to eliminate nearly all of the grunt work that once fell to humans. The agents currently approve 85% of expenses without human review, and early customers report 99% accuracy in expense approvals. The AI doesn’t just process receipts—it cross-references calendar data, checks policy nuances, and delivers outcomes that make sense to human managers.

Zaks’ says this vision is most clearly exemplified by the SMS example. After using his Ramp card, Zaks receives a text asking what the expense was for. The system checks his calendar, sees a scheduled one-on-one meeting, and when he confirms it was for that meeting, the entire expense process completes automatically. No apps to open, no forms to fill, no categories to select.

Managers no longer see dashboards filled with every transaction. Instead, they find two categories: expenses that “look good to go” with a single approval button, and transactions that need attention with focused context about why. Each flagged item includes a summary in 15 to 20 words, the full policy context highlighted on demand, and a feedback mechanism that improves the system’s accuracy.

“It’s not an AI view. It’s like a transaction view. You have the receipt, all the information you need,” Zaks says. “And there’s a module at the top that just says a recommended outcome for the manager to take and the reasoning why.”

Why Ramp exists

Ramp’s move toward the near-total elimination of UX is logical, given the company’s mission. Ramp’s founders, Eric Glyman, Karim Atiyeh, and Gene Lee, all worked in Capital One’s credit card division in the late 2010s. They joined after Capital One acquired their company Paribus, a price-tracking app that secured refunds for 10 million users when online purchase prices dropped.

At Capital One, they realized there was a fundamental tension in the business model: Credit card companies incentivized spending, while businesses desperately wanted to save money. In early 2019, they left the bank to start Ramp.

Ramp’s core premise flipped the script. Instead of rewards programs that encourage more spending, the company built a financial operations platform that actively helps companies spend less while automating the tedious work that consumes finance teams.

For accounts payable, invoices are processed through customizable approval workflows and payments are scheduled automatically. All transactions sync to business management software in real time. Ramp generates revenue primarily through interchange fees earned on every card transaction (typically 1.5% to 2.5% of the purchase value shared among Visa, the issuing bank, and Ramp).

Ramp is now one of the hottest tech unicorns, with a valuation of $22.5 billion after capturing less than 2% of the U.S. corporate card market. The company claims that its customers save an average of 5% on spending, close their books 75% faster, and have collectively saved more than $10 billion and 27.5 million hours of work.

Building an invisible interface

So much of Ramp’s success hinges on the idea that the best AI is the AI you can’t see. Zaks calls this “background” AI, and it’s what will power the next generation of Ramp’s zero-interface ambitions.

Right now, every time a human makes a decision on Ramp’s platform that information is used to create a better experience. When a manager disagrees with an agent’s decision, for example, their explanation is fodder for better policies. The agents can alert teams to suspicious receipts and invoices, uncover trends that signal fraud or careless spending, answer employee questions about spend policy, and suggest edits to company expense policies based on usage patterns.

The experience data aggregates into policy suggestions for finance teams. Zaks explains that the system basically says, “Hey, your policy could be a little clearer about these five things on the work-from-home stipend,” for example. If the finance team agrees, they can approve policy updates with one click.

Eventually, Ramp will be so optimized that its UI will “disappear” in the future. That’s Zaks’s objective: He wants most users to forget Ramp even exists. “My approach has been to just pretend like we’re already in 2030 and that AI is just standard, nobody cares, it’s just always in the background,” he says. “Kind of like how software now is in the cloud. We don’t make a big deal out of that. It just is.”