Want more housing market stories from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter.

Several of America’s largest homebuilders are sounding a cautious note on the 2025 housing market, reporting softer-than-expected buyer demand. The pullback has been especially noticeable across key Sun Belt metros, where affordability pressures are biting.

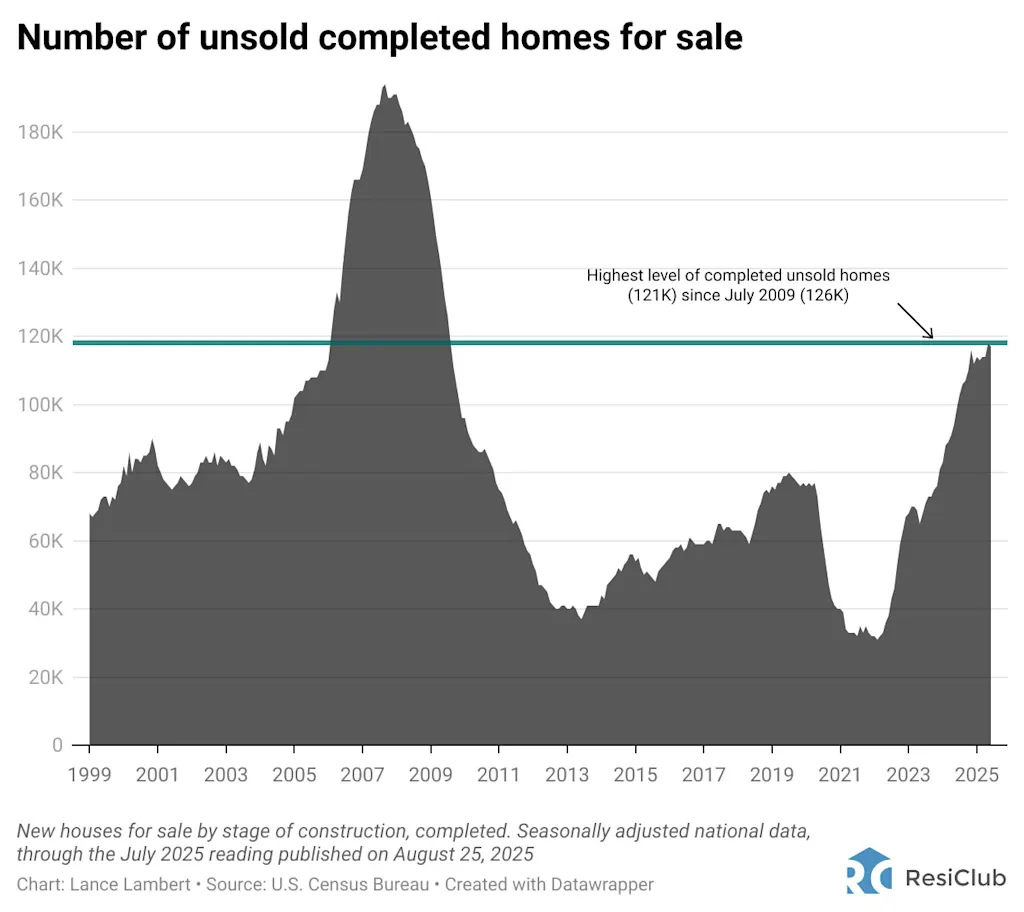

This softer housing demand environment is causing unsold inventory to tick up. Indeed, since the pandemic housing boom fizzled out, the number of unsold completed U.S. new single-family homes has been rising:

July 2016 —> 58,000

July 2017 —> 65,000

July 2018 —> 65,000

July 2019 —> 80,000

July 2020 —> 58,000

July 2021 —> 34,000

July 2022 —> 38,000

July 2023 —> 70,000

July 2024 —> 103,000

July 2025 —> 121,000

The July figure (121,000 unsold completed new homes) published last week is the highest level since July 2009 (126,000).

Let’s take a closer look at the data to better understand what this could mean.

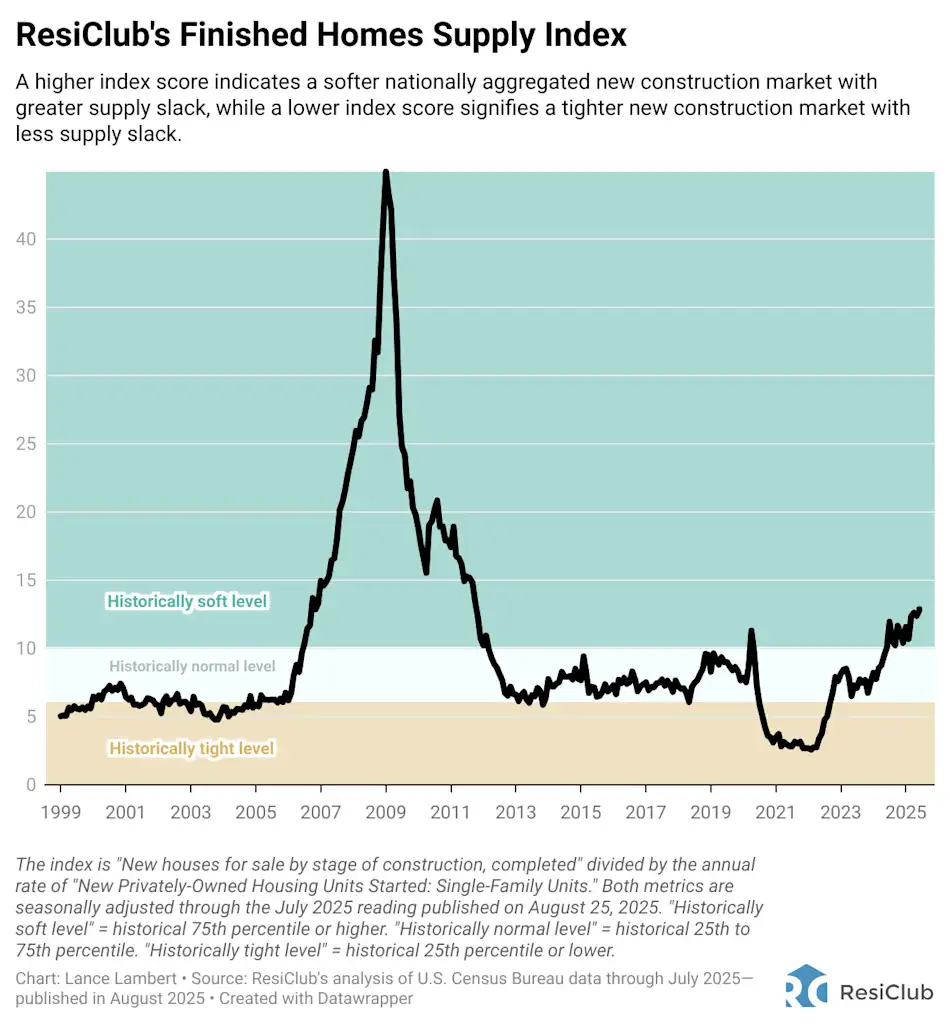

To put the number of unsold completed new single-family homes into historic context, we have ResiClub’s Finished Homes Supply Index.

The index is one simple calculation: The number of unsold completed U.S. new single-family homes divided by the annualized rate of U.S. single-family housing starts. A higher index score indicates a softer national new construction market with greater supply slack, while a lower index score signifies a tighter new construction market with less supply slack.

If you look at unsold completed single-family new builds as a share of single-family housing starts (see chart below), it still shows we’ve gained slack (and have more now than pre-pandemic 2019); however, this slack, nationally speaking, isn’t anything close to the 2007-2008 weakening.

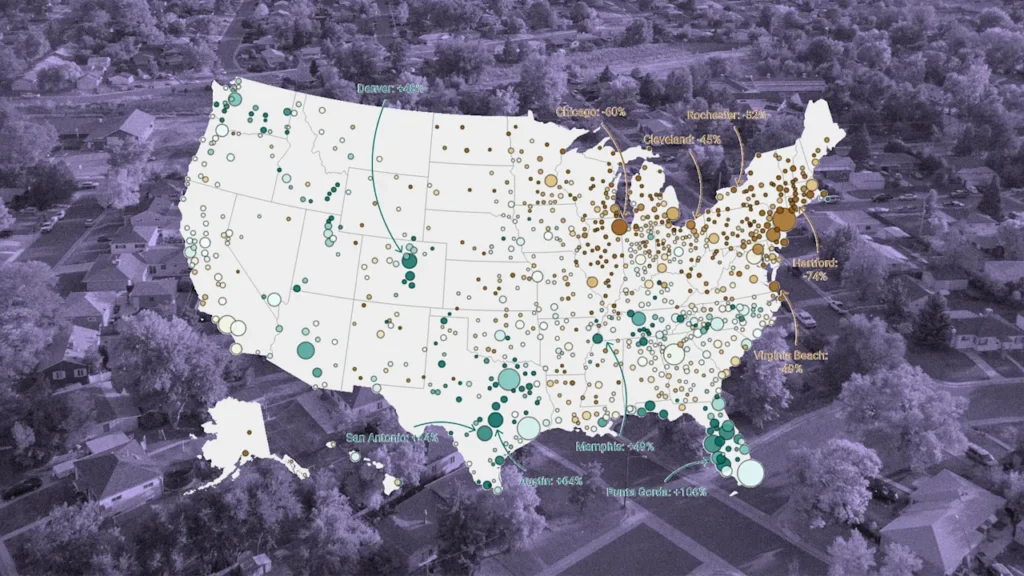

While the U.S. Census Bureau doesn’t give us a greater market-by-market breakdown on these unsold new builds, we have a good idea where they are, based on total active inventory homes for sale (including existing)—likely much of it is in the Mountain West and Sun Belt, particularly around the Gulf.

Indeed, some builders are experiencing pricing pressure, particularly in major markets like Florida and Texas, where resale inventory is well above pre-pandemic 2019 levels.