US retail sales of plant-based meat fell 7.5% to $1.13 billion in the year to April 20, 2025, with units down 10%, according to new data from SPINS shared with AgFunderNews.

Sales of frozen meat alternatives were down 5.3% to $782.3 million, accounting for 69% of category sales, while sales of refrigerated alt meat—a category that has been going backwards since Q3, 2021—fell 12.1% to $349.7 million.

The only subsegments delivering growth over the 52-week period were frozen plant-based loaves and roasts (+0.7%), refrigerated cutlets, strips, and nuggets (+8.3%), refrigerated dogs (+1.9%), and refrigerated seitan (+1.7%), albeit off a small base.

Sales of refrigerated plant-based burgers, which were driving significant growth in the category a few years ago as retailers experimented with merchandising brands such as Beyond Meat in the conventional meat case, continued their precipitous decline, dropping 26% YoY.

For context, Circana data crunched by 210 Analytics shows US retail sales of conventional fresh meat rose 6% over the same period (volumes +2.7%), while sales of frozen processed meat & poultry were up 10.9% (units +10%), and sales of frozen unprocessed meat & poultry were up 4.2% (units +3.3%).

Reduced assortments in US retail

According to 210 Analytics, retailers have been gradually reducing their assortments in the refrigerated alt meat category, with an average of 9.7 items per store in April 2025, down 10.3% since April 2024 and down 31% since early 2021.

Some items have been dropped while others have moved to the frozen set, a trend highlighted by Beyond Meat in its latest earnings call.

US retail sales, 52 weeks to April 20, 2025

-

- Frozen meat alternatives: Dollars -5.3% to $782.3 million, units -7.8%

- Refrigerated meat alternatives: Dollars -12.1% to $439.7 million, units -14.4%

- Total: Dollars -7.5% to $1.13 billion, units -10%

Top four frozen categories:

-

- Nuggets, strips, cutlets: -6.8% to $296 million

- Burgers: -4.1% to $209 million

- Breakfast meat alternatives: -5% to $129 million

- Grounds: -4.7% to $47 million

Top four refrigerated categories:

-

- Grounds: -14.1% to $82 million

- Dinner sausage links: -14.4% to $71 million

- Deli meats: -4.9% to $44 million

- Burgers: -26% to $40 million

Source: SPINS US retail, MULO + convenience, and natural channel, expanded, 52 weeks to April 20, 2025.

Pockets of growth in some plant-based categories in US retail

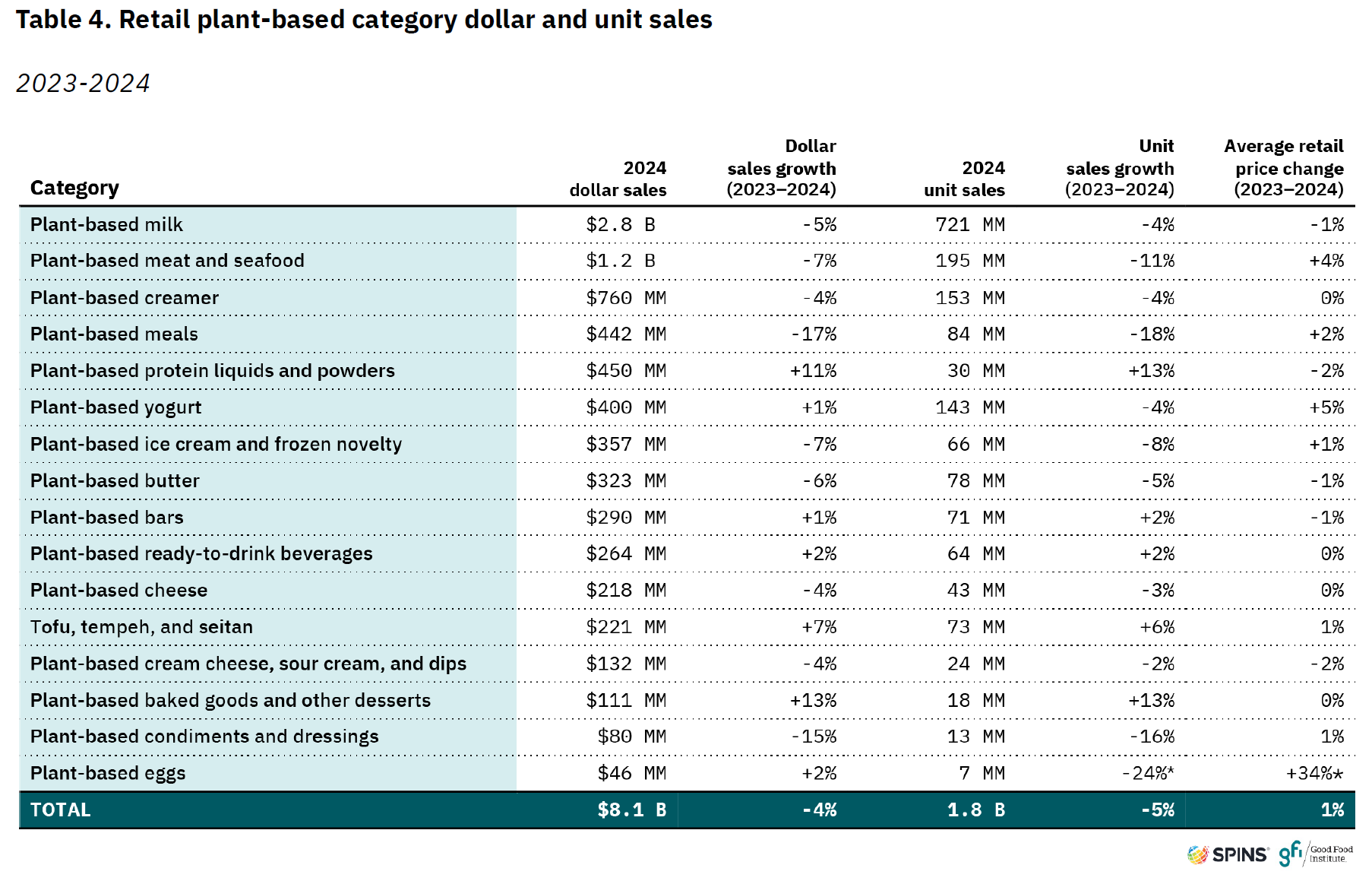

In calendar year 2024, SPINS data analyzed by the Good Food Institute (GFI) and the Plant Based Foods Association in a recent report shows that US retail sales of most plant-based categories were down last year against a backdrop of rising sales for conventional meat & seafood (+4%) and dairy milk (+1%).

According to the GFI, sales of plant-based meat and seafood sales dropped 7% to $1.2 billion in 2024 (units -11%) while sales of plant-based milk fell 5% to $2.8 billion (units -1%). Overall, plant-based food sales at US retail fell 4% to $8.1 billion with unit sales down 5%.

US household penetration has stabilized at around 40% for plant-based milk and 13% for plant-based meat, adds the GFI, noting that pricing for most plant-based categories remains “two to four times higher than conventional counterparts on a per-pound, per-gallon, or per-dozen basis.”

It adds: “Plant-based meat and seafood’s dollar share was 1.7% of total retail packaged meat dollar sales, or approximately 0.8% of the total meat category. In the natural channel, the category’s share of packaged meat dollar sales was notably higher at 8%.”

However, it’s not all doom and gloom, says the GFI, noting that several plant-based categories demonstrated growth in 2024 including plant-based protein powders and liquids, bars, ready-to-drink beverages, tofu, tempeh, seitan, and baked goods and other desserts.

“Despite overall sales declines, the retail plant-based food market showed signs of stabilization and pockets of growth in 2024. While distribution declined across channels, both dollar and unit velocities improved overall and for many categories in both the conventional multi outlet (MULO) and natural channels. While some products were discontinued, others were launched.”

US foodservice sales: Stronger performance in alt dairy offset by weaker sales in alt meat

In the US foodservice sector, which experienced moderate overall growth last year, sales in the plant-based proteins category (meat and seafood analogs, tofu, tempeh, grain/nut/veggie items such as bean burgers) fell 5% in 2024, according to the GFI.

Bright spots included plant-based pork, chicken tenders, chorizo sausage, tofu, and tempeh, which all experienced growth.

Plant-based milk grew in foodservice in 2024, with dollar sales up 9% and volumes up 6%.

Foodservice sales of plant-based egg sales surged 28% in 2024 albeit off a tiny base, adds the GFI. “And they may be poised to capture additional share in 2025 as animal egg prices continue to rise due to increasing rates of highly pathogenic avian influenza.”

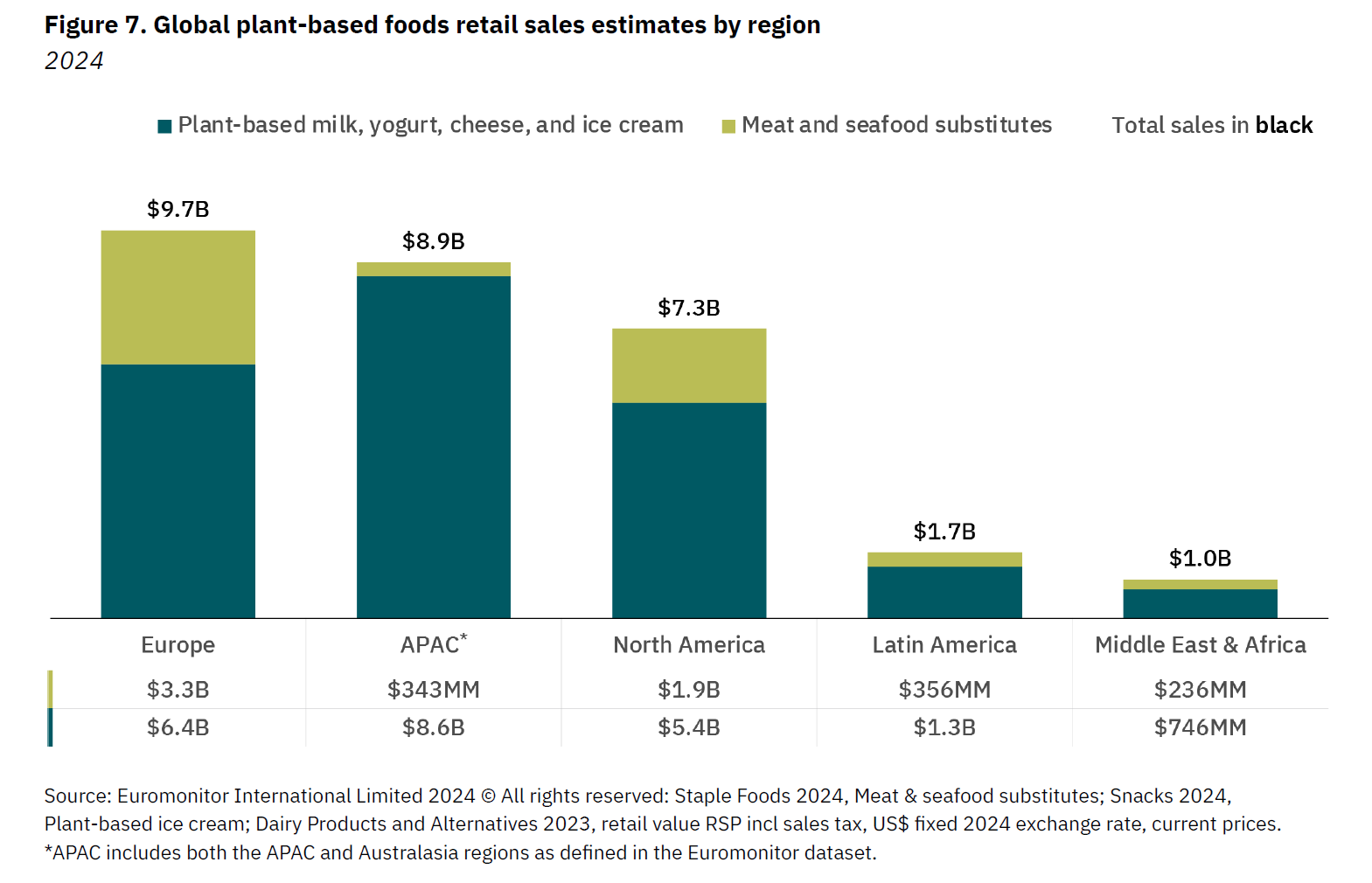

Global retail sales

Citing Euromonitor data, the GFI estimates that global retail sales of plant-based meat and seafood rose 4% to $6.1 billion in 2024, while plant-based dairy sales rose 5% to $22.4 billion.

“Plant-based milk accounted for over 80% of global retail plant-based dairy sales. Plant-based yogurt, ice cream, and cheese remain nascent categories across markets.

“However, growth in the plant-based cheese category (+11%) outpaced the overall dairy category in 2024.”

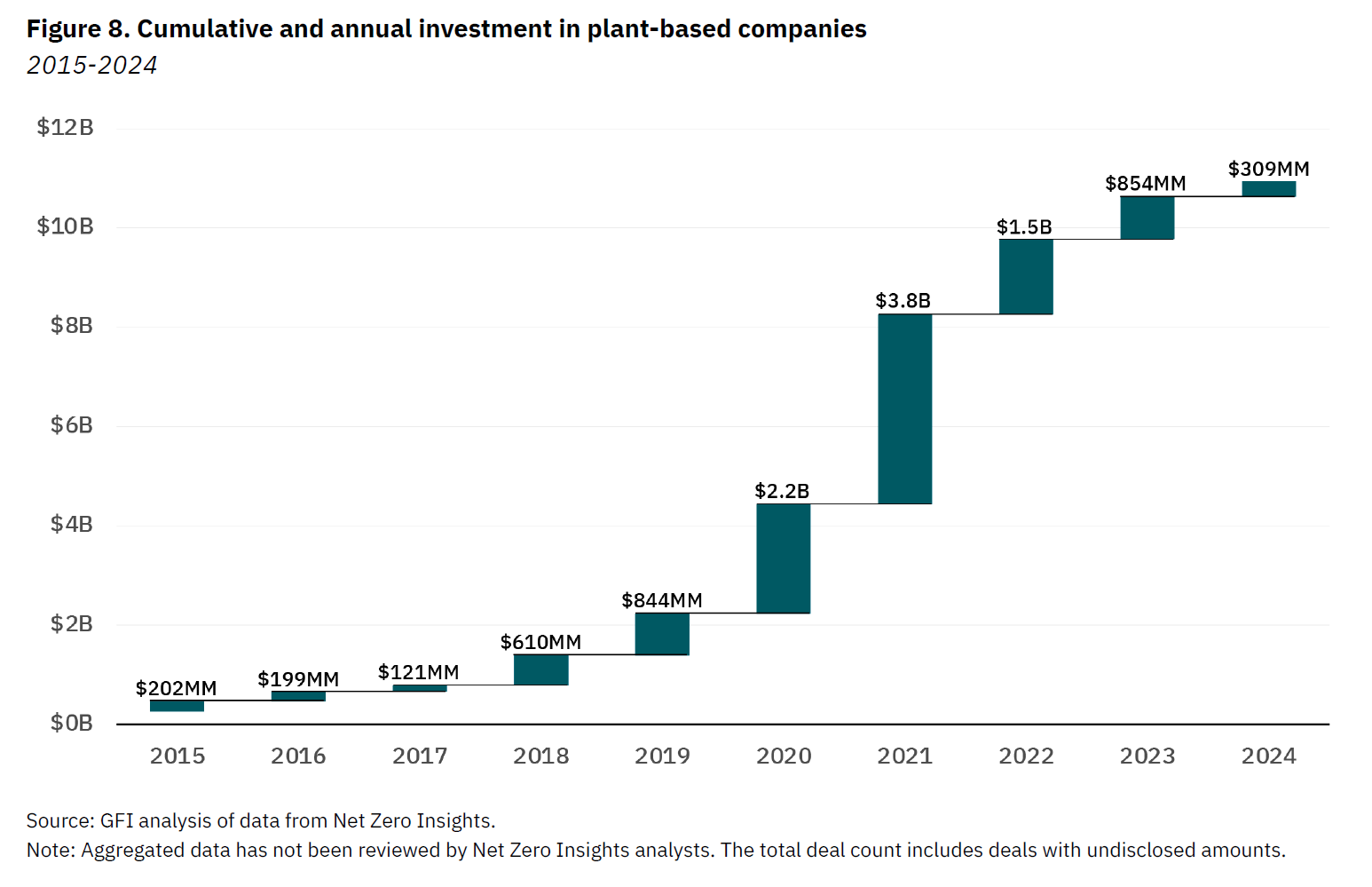

Investment: Funding down 64% to plant-based startups in 2024

Funding for startups making plant-based meat, dairy, and eggs plummeted by 64% in 2024 from $854 million to just $309 million, says the GFI.

“It seems that on average, investments going forward will be distributed to fewer companies and in smaller quantities than during the low-interest-rate environment of 2020 to 2022.”

Without successful exits, it adds, “Plant-based investments will likely remain closer to the levels seen in recent years. Even if the venture market shifts, it is unlikely to soon return to the peak environment of 2021, which was driven by an extended period of near-zero and even negative interest rates following the 2008 financial crisis.”

The sharp drop-off in funding, paired with ongoing sales declines in many regions, means some manufacturers will be unable to secure funding and will downsize, close operations, or merge with other organizations, predicts the GFI.

“But consolidation should not be equated with a weakening plant-based ecosystem. Consolidation is inevitable for any nascent sector, and mergers, acquisitions, and intellectual property transfers can accelerate the dissemination of technology and expertise within an industry.”

The post Plant-based meat by numbers: Grim reading for the US retail market, brighter spots in foodservice and globally appeared first on AgFunderNews.