The insect ag industry is littered with the corpses of startups who found out the hard way that scaling biological systems is not as easy as it looks, prompting a wave of think pieces suggesting its days are numbered.

Despite the sector’s well-publicized struggles, however, its death may well have been exaggerated, say stakeholders we caught up with in recent weeks, who note that no two insect ag operations are quite the same.

As Maiko van der Meer at Dutch black soldier fly larvae (BSFL) specialist Protix recently observed, “When people talk about Ÿnsect’s failures as systemic failures, it always frustrates me. Mealworms [Ÿnsect’s specialty] are not the same as black soldier flies [Protix’s specialty]. It’s like talking about chicken and pigs. If a chicken company goes bankrupt, you don’t say all the pig companies are going to go [bust].”

That said, a string of bankruptcies, restructurings, and stalled projects—from Ÿnsect’s liquidation to ENORM’s collapse and the receivership of Aspire Food Group—has forced a rethink of what scalable, profitable insect agriculture looks like, he concedes.

As Entosystem’s Cédric Provost puts it, “One of the most important learnings for us, and increasingly for the industry, is around feedstock. To build a truly viable and scalable model, insect production needs to be based on residual streams that currently have little to no value or even represent a cost to dispose of.

“This is where the economics start to make real sense. In that context, we see the recent challenges in the insect industry less as a reflection of weak fundamentals, and more as a result of execution complexity, capital intensity, and in some cases feedstock strategies that are not optimized for long-term viability.”

‘European-only model for BSFL production faces nearly insurmountable structural challenges’

And in this respect, geography is emerging as a defining fault line, with EU rules that block insect farms from using post-consumer food waste and most animal by-products as feed making it hard for the numbers to add up, according to Protix, which is now pivoting toward Southeast Asia, where there are fewer feedstock restrictions coupled with cheaper labor, building and energy costs.

Mohamed Gastli, CEO at French firm nextProtein, which is building larger-scale facilities in Tunisia, adds: “We have long believed that the ‘European-only’ model for black solder fly larvae production faces nearly insurmountable structural challenges regarding the cost of feedstock, energy, and labor.

“Our business model—retaining R&D and engineering in Europe while locating production in emerging markets—was designed specifically to solve this profitability puzzle.”

Others, however, argue that tighter regulations on feedstocks permitted in Europe offer a degree of market protection, with French firm Agronutris noting that products entering the EU market must comply with the same standards. “This limits the ability for lower-cost imports produced under less stringent rules to compete directly in the short term,” says general manager Cédric Auriol. “In that sense, European regulation is both a constraint and a form of market protection.”

Frass fertilizer ‘a significant and often underappreciated opportunity’

As for end markets, aquaculture, backyard chickens, and petfood remain key for insect protein and oil, while several firms say insect waste or frass has the potential to play a bigger role. For protein, pricing has to be in the right ballpark to have any kind of conversation, says Oberland Agriscience founder Greg Wanger, PhD. But the conversation is becoming more nuanced as new research comes out on the health benefits of insect ingredients.

“If you’re talking about a direct replacement, it’s very tough to compete against soy. But there are anti-inflammatory and anti-microbial benefits to the animals and growth benefits that you get with black soldier flies.

“Once you start to talk to operators of aquaculture facilities, for example, and you ask: What is it worth to you if we can reduce mortality? What if you don’t need to use antibiotics? Then you can see the narrative start to change, because up until now, we didn’t really have the data to back it up.”

Frass, in turn, “represents a significant and often underappreciated opportunity,” claims Provost at Entosystem. “We’ve funded multi-year studies demonstrating its biostimulant properties and its positive impact on soil health and plant performance. We believe this is a high-value product that is currently underestimated by the industry, particularly in the context of regenerative agriculture.”

Checkout our updates with some key players below to get a sense of where the sector is heading.

👉 nextProtein (BSFL, France/Tunisia): R&D/engineering in Europe, production in emerging markets

nextProtein raised €18 million ($21 million at the time) in late 2025 to scale production in Tunisia, betting that lower-cost feedstocks and lower capex and opex will enable it to deliver insect protein at competitive prices, says CEO Mohamed Gastli.

“We are currently in the final installation phase at our second production site, which is on track to be operational by Q4 2026 and will have an annual capacity of 2,500 tons of protein meal.

“For feedstock, we utilize a blend of organic agricultural and agri-food byproducts perfected over several years. We consider our feedstock strategy to be the most advanced in the sector; it delivers industry-leading conversion rates while remaining in full compliance with stringent European safety and quality legislation. Our expertise lies in transforming organic waste into a standardized, high-performance input.”

Aquaculture remains the firm’s primary market, he says. “However, since 2025, we have seen a significant surge in commercial appetite for our insect oil and frass [as fertilizer], as industries look for sustainable alternatives to vegetable oils and chemical fertilizers.”

He adds: “We are not surprised by Protix’s comments; in fact, they validate the strategic vision nextProtein has held for a decade. We have long believed that the ‘European-only’ model for BSFL production faces nearly insurmountable structural challenges regarding the cost of feedstock, energy, and labor.

“Our business model—retaining R&D and engineering in Europe while locating production in emerging markets—was designed specifically to solve this ‘profitability puzzle.’ By combining European precision engineering with the competitive Opex and Capex environments of regions like Africa, Asia, or the Americas, we can achieve the unit economics required to truly scale. We believe the future of the industry belongs to those who can produce a high-quality product at a price point that is competitive with traditional proteins.”

👉 Entobel (BSFL, Vietnam): ‘We underestimated the difficulty coming with the production of insects at scale’

“We faced a challenging commissioning period in early 2024 as we started ramping up our newly built factory in Southern Vietnam,” says cofounder Alexandre de Caters. “Despite having five years of industrial track record at that time, as we have been producing at commercial scale since 2019, we had our fair share of technical issues. Like many of our peers, we underestimated the difficulty coming with the production of insects at scale.”

Most of those challenges were resolved by the end of 2024, he claims, and Entobel is now “routinely producing” 300 to 400 tons of insect meal a month alongside frass and oil. “Having stabilized our ramp-up, we decided to try and become the global industry cost leader, and have since been focusing relentlessly on production cost optimization,” he adds. “In December 2025, we achieved a production cost milestone allowing us to sustainably develop feed applications.”

The decision to set up in Vietnam more than a decade ago is starting to pay off, he adds. “We are growing a tropical insect in its natural environment. Our tech has been designed in-house to leverage local weather conditions while maintaining a low CAPEX intensity. Our energy consumption is low, which is also helping us to achieve low carbon footprint levels. This cost structure is a significant competitive advantage and, in our opinion, the best way to develop aquafeed applications that are financially sustainable.”

In 2024, Entobel established a research facility in Sumatra, Indonesia, to investigate the viability of palm oil waste and by-products as feedstock, he says. “We are now confident that this model offers very significant growth potential. We are also engaging with various potential partners in other tropical and sub-tropical regions of the world, as we aim to replicate the success of our Vietnamese business model.

“Even though our expansion’s timeline has shifted, the long term potential of the industry remains unchanged.”

👉Agronutris (BSFL, France): European regs ‘both a constraint and a form of market protection’

Agronutris, which filed a safeguard plan with a commercial court in January 2025, has since secured additional funding, says general manager Cédric Auriol. “This allows us to resume our development trajectory with a clearer and more disciplined approach.”

“It is true, as highlighted by Protix, that Europe currently restricts the use of certain post-consumer waste streams and animal by-products as feedstock,” says Auriol. “This impacts cost competitiveness versus regions such as Southeast Asia.

“However, this regulatory framework also creates a level playing field within Europe. Products entering the European market must comply with the same standards, which limits the ability for lower-cost imports produced under less stringent rules to compete directly in the short term. In that sense, European regulation is both a constraint and a form of market protection.”

He adds: “We broadly share the view that large-scale, highly automated industrial models are more challenging to make competitive in high-cost regions such as Europe or North America. As a result, we expect future capacity additions to follow two complementary paths:

- More decentralized or modular approaches in developed markets, closer to feedstock sources

- New large-scale facilities in emerging economies, where structural costs (labor, energy, capex) and regulatory frameworks are more favorable.”

“That said, building new industrial capacity takes time everywhere and existing European assets must continue progressing toward profitability in order to keep serving both current and growing markets.”

One key evolution for the sector is the shift from purely commodity-driven positioning toward higher-value applications, he adds. “Scientific progress is increasingly demonstrating that insect-derived ingredients can deliver functional benefits such as improved animal health, immunity, and performance. This opens the door to more specialized, higher-value markets beyond simple protein substitution.”

For European producers in particular, this move up the value chain will be critical to achieving sustainable profitability, he claims.

Looking ahead, he says, “A gradual expansion of the authorized feedstock base would be a key unlock for the industry in Europe, where insect-derived products are already being used at scale across pet food, aquaculture, livestock nutrition, organic fertilization, and energy applications.”

👉 Volare (BSFL, Finland): Offtake deal with Skretting

Volare—which raised a €26 million round in 2025—is building a 5,000-ton (dry protein meal) production facility at a brownfield site in Pori, Finland having validated its tech at a demo-scale site, says CEO Jarna Hyvönen.

“We are already quite close to finalizing installations and starting the ramp-up phase. We have an offtake agreement and great collaboration with [aquafeed giant] Skretting. We’ve also done a commercial launch of rainbow trout feed with [Finnish feed producer] Alltech Fennoaqua. The BSF meal has been shown to work very well in aquafeeds in various species and it has already been used in commercial applications for years. What I see is that the demand is there as long as the key criteria of customers are met: high digestibility, realistic cost-structure and ability to deliver.”

Pet food producers in Europe are interested “as long as ingredients are of high quality and there is security of supply,” she claims. “When it comes to the oil, the markets are in an interesting situation due to new regulations affecting other markets using the same oils as pet foods and feeds. This is putting pressure on the availability of oils for all the industries that need them, including chemicals, biofuels and feeds [and potentially making insect oil more competitive].”

As for restrictions on feedstocks for insects in the EU, she says, “Over time, we see that the rules can be loosened… however, our business model is not based on this change. Although feedstock plays an important role in cost structure, you can affect other major cost items by smart choices in power supply and usage, labor needs, and the factory’s wastewater costs, thereby reducing unit costs, and continue to serve customers who are de-risking their supply chains by sourcing from Europe.”

According to Hyvönen, firms building plants today have learned from the mistakes of the pioneers in the space. “It doesn’t make sense to reinvent the wheel and having as much as fancy technology as possible is not the point. The point is to make it efficient and make it work, so there are things that definitely make sense to automate, but not all of the process, for example.”

“We have a specific dry process for protein meal production that reduces energy usage by about 30% and we’ve figured out a process to hygienize the frass where we use about 50% less energy.”

For customers in aquafeed, she says, “Security of supply is a big thing and insect ag is closer to scaling than many of the other novel protein solutions. When it comes to product quality, it’s about digestibility, palatability, and health benefits as well as price and availability.”

👉 Entosystem (BSFL, Canada): Lower-cost feedstocks are pivotal to commercial success

According to president Cédric Provost, “One of the most important learnings for us, and increasingly for the industry, is around feedstock. To build a truly viable and scalable model, insect production needs to be based on residual streams that currently have little to no value or even represent a cost to dispose of.

“This is where the economics start to make real sense. In that context, we see the recent challenges in the insect industry less as a reflection of weak fundamentals, and more as a result of execution complexity, capital intensity, and in some cases feedstock strategies that are not optimized for long-term viability.”

Since its CAD$58 million ($42 million) funding round in 2024, Entosystem has made progress scaling operations at its Drummondville black soldier fly larvae facility in Quebec, and is evaluating options for a second site in the US.

“From the start, we have focused on building our model around pre-consumer food waste streams that are safe and traceable, but that would otherwise be destined for landfill,” he says. “This approach is central to what we do. It allows us to combine strong unit economics with a meaningful environmental impact, which we believe is essential for long-term success in higher-cost markets.”

Right now, its primary market is the backyard chicken market, “where we’ve developed a strong value proposition around premium treats,” he says. “This segment has proven particularly attractive, and our white-label offering is gaining traction with several large retail chains looking for differentiated, sustainable products.

“Looking ahead, we’re seeing increasing demand from additional segments. Pet food, particularly in the US, continues to build momentum. At the same time, interest from the aquaculture sector in North America is accelerating, representing a newer source of demand for us. We are now seeing similar dynamics to what first emerged in Europe, with strong interest driven by both sustainability and performance. The positive impact on animal health at low inclusion rates makes integration easy for aquaculture players, without requiring major formulation changes, while reducing reliance on marine-based ingredients remains a key driver.”

Frass, in turn, “represents a significant and often underappreciated opportunity,” he claims. “We’ve funded multi-year studies demonstrating its biostimulant properties and its positive impact on soil health and plant performance. We believe this is a high-value product that is currently underestimated by the industry, particularly in the context of regenerative agriculture.”

👉 Innovafeed (BSFL, France): US plans ‘very much alive’

Innovafeed says its large-scale black soldier fly larvae (BSFL) facility in Nesle, France, is on track to be profitable by the end of 2027, with customers in aquaculture and pet food, and insists that plans to build a commercial-scale facility next to an ADM corn milling plant in Decatur, Illinois, are “very much alive.”

“We focus in the short term on accelerating the commercial development of our Hilucia ingredients, particularly in the US pet food market.”

The company—which uses wheat byproducts from a co-located Tereos starch processing plant to feed its BSFL at its French facility—has been testing corn byproducts from ADM as feedstock for the US plant.

“Over the past 18 months of pilot operations, we generated promising R&D results confirming the potential of locally sourced corn co-products as a substrate for insect rearing,” says a spokesperson.

“We remain confident in the long-term potential of insect ingredients,” adds the firm, which cites recent partnerships with BioMar, Auchan, and NaturAlleva for aquaculture, with additional announcements in petfood to follow.

👉 Protix (BSFL, Netherlands): ‘We’re heading east…’

Dutch insect farming pioneer Protix is pivoting to Asia, arguing that lower costs and more favorable regulations make the region a better fit for scaling insect protein production than Europe or North America.

CEO Maiko van der Meer says strict EU rules on feedstock make it difficult for facilities in countries such as the Netherlands and France to compete economically. In contrast, Southeast Asia offers cheaper land, labor, energy, and construction costs, fewer feedstock restrictions, and warmer climates that reduce the need for energy-intensive climate control.

Moving forward, Protix’s black soldier fly larvae facility in the Netherlands will increasingly function as a technology and development hub rather than a long-term production center, while plans for a plant in Poland have been shelved. In North America, the company has completed designs and technical work for a proposed large-scale facility in Nebraska with Tyson Foods, but says the project is currently on hold.

👉 Chapul Farms (BSFL, US): North Dakota plans ditched in favor of smaller Oregon plant

Chapul Farms has ditched plans to build a large-scale black soldier fly larvae plant next to a corn ethanol plant in North Dakota and pivoted to a smaller commercial facility in McMinnville, Oregon, with phased construction designed to reduce upfront risk, says founder Pat Crowley.

Unlike the shelved North Dakota plan—which relied on a much larger capital stack and ultimately stalled because Chapul could not secure a lead equity partner—Oregon is smaller, closer to the team’s base, and easier to finance in stages, he says.

The Oregon plant—formerly a plastics plant—will process a blended feedstock of landfill-diverted food waste and dry bakery waste used to fine-tune moisture levels, explains Crowley, who says the broader insect farming ecosystem has matured significantly in terms of equipment, air handling, and operating know-how, even if capital remains hard to access after several high-profile failures in the sector.

Stepping back, Crowley says the sector’s setbacks are not due to one single flaw, but to a mix of over-ambitious business models, weak capital alignment, and in some cases excessive spending on automation.

Even so, he remains “a prisoner of hope,” adding: “I have viewed insect agriculture as having three pillars: waste management, protein/fat production, and frass production. If a model is designed to optimize for one, like many European protein-factory models, the other two suffer and the system/business is less resilient to disruption from the supply chain and the market.

“Five years ago I saw the frass market as one of the more undeveloped and we have put a lot of our resources into building frass markets and discovering the tremendous role it plays in soil health.”

👉 FreezeM (neonates, Israel): A maturing ecosystem

An Israeli startup with a breeding-as-a-service model that supplies black soldier fly neonates to the insect farming industry, FreezeM says it has 40 customers right now in various stages of development.

On the market side, cofounder and CEO Yuval Gilad PhD says there is still meaningful activity despite lower visibility, with mid-scale projects emerging across Europe, the UK, Canada, the US, Israel, and especially China, where he says government support is helping drive expansion.

In future, predicts Gilad, the industry will move away from the capital-intensive, vertically integrated mega-factory model pursued by many first-generation players and toward smaller, more modular, more commercially grounded facilities, a shift enabled by a more mature ecosystem of equipment and technology providers.

👉 Aspire Food Group (crickets, Canada): Receivership

Billed as the world’s largest cricket processing facility, Aspire’s highly-automated facility in London, Ontario, ran into serious trouble last spring with receiver FTI Consulting blaming its underperformance on

(a) geographical and environmental differences between the growing process in Texas, where the process was developed, and Ontario, where Aspire sought to scale up

(b) changes in growth and harvest methods such as a new tote design and stacking system

(c) problems with the hopper and conveyor systems.

In September, the Ontario Superior Court of Justice approved a deal to sell its assets to Halali Group Holdings, a purchaser with “interests in commercial real estate and food and beverage manufacturing.”

Court documents filed by FTI indicate that Halali “intends to explore opportunities to source a commercial tenant for the London facility so that it will continue to be used for industrial purposes, including, potentially, the insect agriculture business.”

Asked whether the company had erred in building a large automated facility around a design that had worked at a small scale in Texas but had not been properly validated in Ontario, former CEO David Rosenberg said: “You can always be the Monday morning quarterback. If you go from small to medium to big, there’s, let’s say, another 10 to 20 million of expense in that medium term. If you go straight from small to big, there might be 10 to 20 million of expense in all the mistakes you need to fix.”

COO Gabe Mott has not responded to a request for an update on the plant’s current status.

👉 Cricket One (crickets, Vietnam): ‘The market is not yet ready to absorb large volumes of cricket protein’

“2025 has been quite a turbulent year for the insect protein space overall, but we’ve seen some encouraging developments on our end,” says cofounder Nam Dang.

“In Vietnam, our consumer-facing cricket food brands have been performing well and growing. Across products like crackers, instant ramen, and pasta, we sold over 1,000,000 units last year. We’re currently projecting between 2–3 million units in 2026, alongside expanding our product range with more variety.

“Globally, the picture has been more mixed. In the US, the cricket-based pet food segment slowed down last year, partly due to tariff uncertainties, which led several manufacturers to pause planned product launches. In human food, the broader insect protein category has faced challenges, with a number of venture-backed players exiting the market. That said, more mature and disciplined companies are still operating and pushing forward.

“On a more positive note, we’re seeing steady and growing demand in certain niche segments, particularly in small pet and aquaculture food, which continue to show strong fundamentals.”

Looking ahead, he says, “Our view is that the market is not yet ready to absorb large volumes of cricket protein at scale. To unlock further growth, we believe companies like us need to actively build the market. For Cricket One, that means going further downstream—expanding retail product lines (like our RecRec brand) and potentially exploring new formats such as restaurants or broader consumer/industrial businesses that incorporate cricket protein as a core ingredient.”

👉 ENORM (BSFL, Denmark): bankrupt

Danish BSFL co ENORM was declared bankrupt in November. The firm, which raised €50 million ($57 million) from backers including Danish ag co-op DLG in 2022, opened a factory in Jutland in 2023 to supply the animal feed market but said momentum had since “waned significantly.”

👉 Inseco (BSFL, South Africa): ‘We scaled too quickly and pivoted too slowly’

Inseco ceased operations last year after running into a series of operational challenges, the most damaging being four-hour power outages that went on for months, says cofounder Simon Hazell.

“We had back-up power installed on site that powered certain equipment such as colony ventilation on an essential circuit. We could not run energy-intensive areas of the plant under this configuration, but it kept our essential operations intact. We mistakenly assumed that loadshedding would not intensify the way it did, and therefore we deferred the purchase of a large genset [generator system] that could power most of the plant.

“However, loadshedding did intensify, and the power outages increased. The essential areas of the plant such as colony and growing took severe strain as temperatures began to fluctuate. We could also not run processing for extended periods. The irony was that we eventually did secure a large genset. It was useful for a few months, and then loadshedding was suspended and has not come back since.”

However, power outages were not solely to blame for the firm’s problems, says Hazell, who said Inseco had made some bad hires, scaled too quickly and pivoted too slowly.

“We were working on a technology that would enable us to generate better margins from the insect biomass. We should have doubled down on this sooner. We got close but ultimately ran out of time.”

👉 Full Circle Biotechnology (BSFL, Singapore/Thailand): ‘Disciplined scaling’

A startup based in Singapore with operations in Thailand, Full Circle Biotechnology is building a 7,000-ton/year insect protein facility in Kanchanaburi, north-west of Bangkok, says founder Felix Collins. “We remain focused on disciplined scaling, with unit economics tracking in line with expectations.

“Today, over 80% of our customers are shrimp farms, where the focus is ultimately very simple: performance and cost. What we are consistently seeing is that feed incorporating Full Circle can reduce cost by around 4–8% versus comparable formulations, while also supporting improvements in growth rates, feed conversion, and key health indicators.

“Importantly, these results are coming through in real farm conditions rather than controlled trials, and we are continuing to build a robust dataset across different geographies and production systems.”

Full Circle’s protein meal is distinct in the segment as it combines black soldier fly larvae and microbial protein produced via solid state fermentation (microbes feeding on organic waste). According to Collins, the feed can “replace up to 75% of fishmeal in aquaculture, the highest commercial substitution rate to date.”

While some players in the space argue that high levels of automation are essential to make the unit economics of industrial scale insect farming add up, Collins says “semi-automated facilities have been most effective in our experience. Avoiding full automation allows for fewer staff while keeping capex down and enhancing quality assurance touchpoints, which is more appropriate for earlier stage companies.”

👉 Loopworm (silkworms, India): Silkworm protein business already profitable

Loopworm is ramping up production at a facility in Bangalore that will be capable of churning out 6,000 tons of silkworm protein meal a year and working in parallel on a platform using silkworms as mini bioreactors to produce recombinant proteins.

Rather than farming silkworms, Loopworm is processing silkworm pupae, a byproduct of the silk industry, supplied by a network of established insect farmers into protein meal and oil. It is already making a profit from this side of its operation, says cofounder Ankit Alok Bagaria, who is sending commercial shipments into Japan, recently opened Kenya as a new market, and is preparing to restart business development in the US as tariff conditions become clearer.

The company’s main focus remains aquaculture, serving segments including shrimp, salmon, yellowtail, and tilapia, where its silkworm oil is increasingly being used not just as an energy ingredient but as an additive to improve palatability and feeding activity, especially in crustaceans. Its protein meal is benefiting from rising fishmeal prices and what the company claims is a stronger amino acid and lipid profile than black soldier fly meal.

While many players in the segment are struggling, Loopworm’s relative success comes down to its business model, geography, and species choice, says Bagaria, who believes insect protein is fundamentally a tropical developing-country play, not a temperate developed-country one, because the economics hinge on climate, labor, land, utilities, and feed.

In his view, many Western insect startups struggled because they were forced into high automation, expensive climate control, and high capex, while companies in India, Southeast Asia, Africa, and LATAM can operate with lower-cost, semi-automated systems.

On the recombinant protein side, Loopworm has gone from a small lab effort to a much bigger strategic push, supported by a dedicated fundraise in 2025. Rather than developing genetically modified silkworms that pass on their capability to express recombinant proteins to their offspring, Loopworm is using transient expression systems. Here, silkworms are injected with viral vectors enabling them to produce the target proteins before they are processed a few days later.

The company sees two routes to market: a push model, where it builds its own catalog of proteins for sectors such as diagnostics, and a pull model, where it works as a CRO/CDMO for partners with specific protein needs. To fund the next stage, Loopworm is preparing a Series A round of $8–10 million to build a commercial recombinant protein facility, expand R&D and IP, and establish business development bases outside India.

👉 Oberland Agriscience (BSFL, Canada): Positive market pull

Canadian insect ag startup Oberland Agriscience has started shipping commercial quantities of protein and frass from its facility in Halifax, Nova Scotia, and appointed food industry veteran Jon Getzinger as CEO as it moves into a new phase of development.

“If you’re talking about a direct replacement, it’s very tough to compete against soy,” says founder Greg Wanger PhD. “But there are anti-inflammatory and anti-microbial benefits to the animals and growth benefits that you get with black soldier flies.

“Once you start to talk to operators of aquaculture facilities, for example, and you ask: What is it worth to you if we can reduce mortality? What if you don’t need to use antibiotics? Then you can see the narrative start to change, because up until now, we didn’t really have the data to back it up.”

He adds: “We’re seeing very positive market pull right now for the protein and the frass [insect waste] as soil health becomes more important. For the protein, poultry is the largest growth industry for us right now, but we’re also talking to companies in petfood and aquaculture.”

As for scaling up, the key to success is ironing out problems at a small scale before you end up spending huge sums on scaling something that won’t work, says Wanger, who feeds his BSFL spent brewers’ grains and fruit & veg waste from large processors.

“One thing we [as an industry] all struggle with is climate control. Black soldier flies like to be at 28⁰C or even hotter, and I can tell you right now it’s not 28 degrees right now in Halifax, so climate control is really important.

“When I started the pilot facility, it was all about energy, so we recapture the heat that we’re generating in one part of the facility and use that to heat the rest of our building. So that works in Halifax, but if we were in Texas or California, where heat is not an issue, you have the reverse problem. I think a lot of people didn’t really understand how much heat or ammonia and other things that these larvae produce.”

👉 Ÿnsect (mealworms, France): Judicial liquidation

Founded in 2011 by Antoine Hubert and Alexis Angot, Ÿnsect honed its mealworm farming process at a pilot facility in Dole, eastern France and started protein production at a larger facility in Amiens, northern France, in 2024, but has proved unable to raise the funds to get it to commercial scale.

The company, often seen as a proxy for the wider sector—which frustrates some players that say mealworms ad BSFL are very different beasts—went into judicial liquidation in December 2025.

👉 Tebrio (mealworms, Spain): Modular and phased development

Mealworm farmer Tebrio, which raised €30 million ($32.6 million at the time) in 2024 to construct a 10,000/t/year facility in Salamanca, Spain, did not respond to requests for an update, but emphasized the “stability and solidity” of its business model” in a recent LinkedIn post.

“Tebrio is committed to a modular and phased development model, which allows progress to be made in a progressive and controlled manner, reducing risk and optimizing the use of resources. Our growth plan is contingent on compliance with a solid business plan, which implies less need for initial investment and the proper alignment between expansion and profitability.”

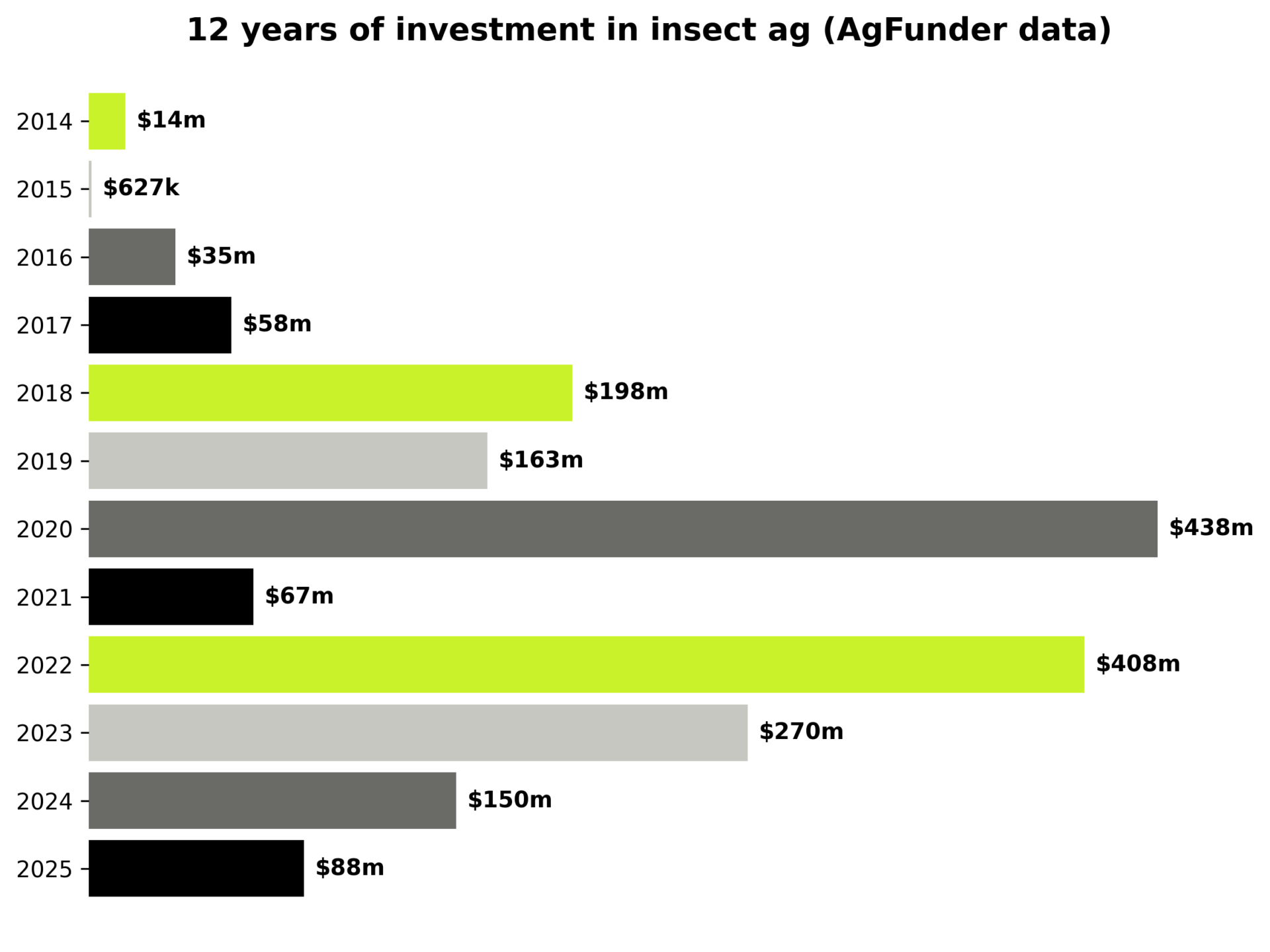

Recent funding rounds in insect agriculture (US dollars):

2025: $87.75 million

- Volare (black soldier fly larvae, Finland): $30 million

- nextProtein (black soldier fly larvae, France/Tunisia): $21 million

- Protix (black soldier fly larvae, Netherlands): $11 million/debt

- Proteine Resources (lesser mealworms, Poland): $11.1 million

- GreenGrahi (black soldier fly larvae, India): $3.7 million

- Loopworm (silkworms, India): $3.25 million

- Insectius (black soldier fly larvae, Spain): $2.9 million

- BetaBugs (black soldier fly genetics, Scotland): $2.7 million

- InsectBiotech (black soldier fly larvae, Spain): $1.7 million

- Enthos Circular Feed Technologies (black soldier fly larvae, Colombia): Undisclosed

- FlyBox (black soldier fly larvae, UK): $400k

2024: $150.2 million

- Entosystem (black soldier fly larvae, Canada): $42 million

- Protix (black soldier fly larvae, Netherlands): $40 million

- Tebrio (mealworms, Spain): $32.6 million

- FreezeM (black soldier fly neonates for breeding, Israel): $14.2 million

- Chapul Farms (black soldier fly larvae, US): $9 million

- Nasekomo (insect ag franchisor, black soldier fly neonate supplier, Bulgaria): $8.7 million

- Entocycle (enabling tech for insect ag, UK): $2.6 million

- Insectius (black soldier fly larvae, Spain): $1.1 million

Source: AgFunder data [disclosure: AgFunder is the parent company of AgFunderNews

The post Insect ag recalibrates after a brutal shakeout: Where are the key players now? appeared first on AgFunderNews.